You know what type of bathroom remodel you need, but you’re not quite sure how it will fit into your budget. You’ve read a little bit about bathroom remodel financing, but how does financing come into play for homeowners who have poor or fair credit? Is now really the right time to take on debt with interest, or should you work on your credit score before your bathroom remodel?

At ZINTEX Remodeling, we’ve worked with thousands of homeowners to create the bathroom remodeling solutions that work best for them, and that includes the financial side. As a result, we understand that sometimes, it’s in a homeowner’s best interest to improve their credit before we build their new bathroom. Are you one of those homeowners? If so, how can you start working on your credit? Read on to find out.

Table of Contents

- Why Does My Credit Score Matter in a Home Remodel?

- What Other Factors Impact My Financing Options?

- What Credit Score Is Considered Poor?

- Should I Take Advantage of a Zero-Interest Loan?

- How Can I Improve My Credit Score Before a Remodel?

Why Does My Credit Score Matter in a Home Remodel?

When a bathroom remodeling company talks about financing options, they’re talking about loans. Many remodel companies partner with lenders, and that partnership might make it a little easier for customers to qualify. However, the same conditions that you could expect when applying for a standard loan still apply.

Ultimately, your credit score will determine:

- Whether or not you will qualify (aka be approved) for financing

- The terms of your loan (e.g., how many months you’ll have to pay it off)

- How high your interest rate is

The better your credit score, the better your financing options will be. For example, you may qualify for a zero-interest or deferred-interest loan. You may also have more flexibility in how much you need to pay each month and how long you have to pay off the full amount.

What Other Factors Impact My Financing Options?

Your credit score isn’t the only thing lenders will consider when setting the rates and terms of your remodel financing loan. They will also look at:

- Your debt-to-income (DTI) ratio: How much of your income is already tied up in paying off existing debt. A low DTI signals that you have more capacity to take on new debt.

- Income stability: How reliable and consistent your monthly or annual earnings are. A stable income makes it easier to estimate your ability to pay off a new loan.

- Project scope: How well the scale (and cost) of your remodel aligns with your current buying power. Lenders may be reluctant to provide financing for a large and expensive project if things like your credit score and debt-to-income ratio are considered poor.

What Credit Score Is Considered Poor?

When you have a poor credit score, lenders are more reluctant to provide you with a loan. This is because at least in theory, credit scores reflect your history of paying off debt in the past. A poor credit score might signal that you’ve:

- Missed loan payments or had a habit of making payments past their deadline

- Filed bankruptcy

- Utilized credit cards at a rate that is considered “high”

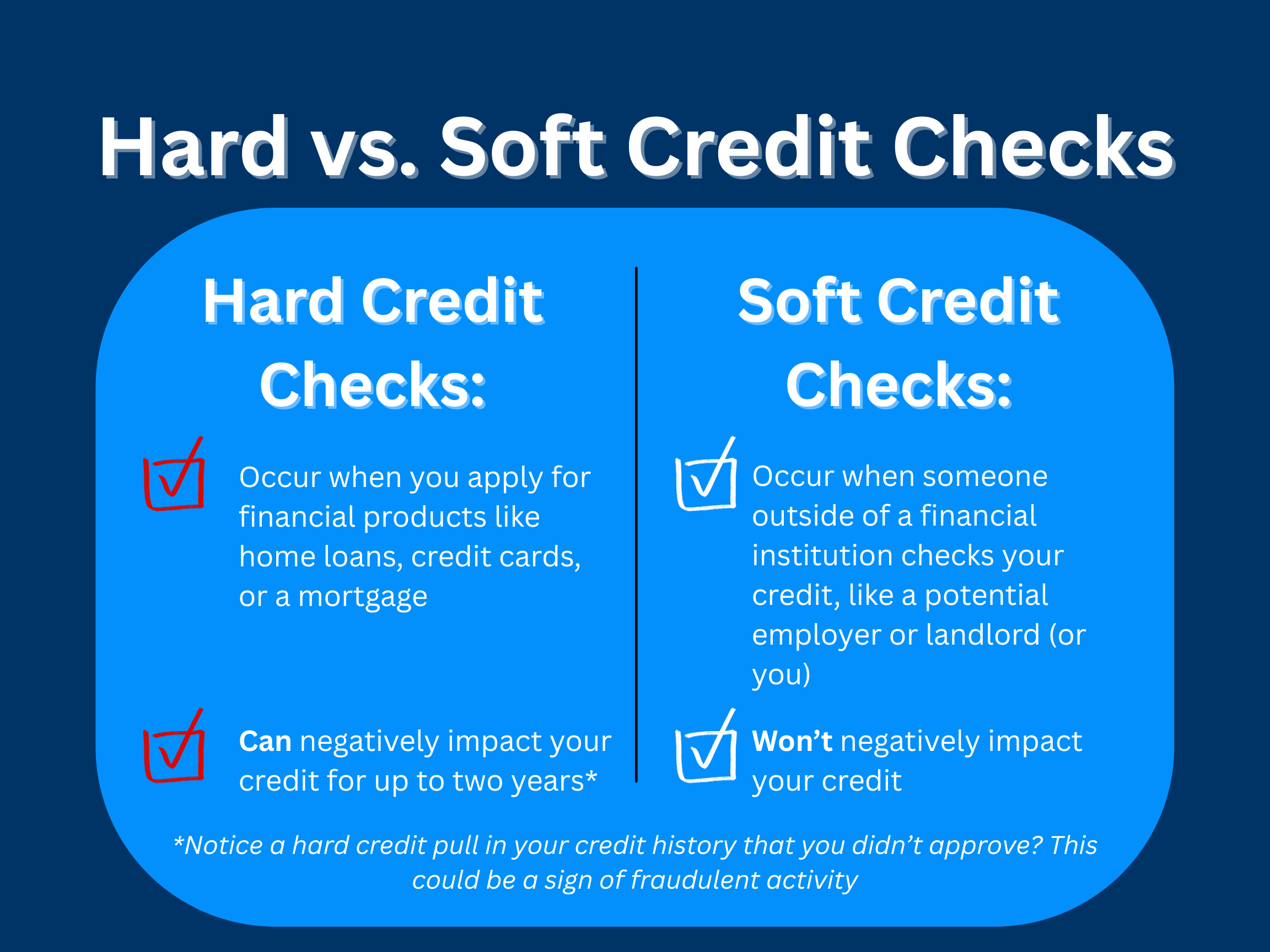

- Had too many hard credit checks (which may happen if you have opened several credit cards or loans back-to-back)

There are multiple creditors that assess credit scores, and they use different ranges to calculate credit scores. For example, FICO scores credit on a scale of 300-850:

- Poor credit: 300-579

- Fair credit: 580-669

- Good credit: 670-739

- Very good credit: 740-799

- Exceptional credit: 800-850

To get the best financing terms for your bathroom remodel, you want to fall into the good or higher range (670-850). However, even homeowners with a credit score as low as 600 may qualify for a zero-interest loan, so long as they meet certain criteria.

Should I Take Advantage of a Zero-Interest Loan?

Many financing institutions will offer a zero-interest home loan to certain borrowers, including those with credit scores in the fair range. You’ll typically have 12-24 months to pay off your loan without interest. If you don’t pay off the total principal amount in that time, the remaining balance will start accruing interest.

This is a great option if you don’t have the best credit, but you do have the cash on hand to pay off your remodel. The benefits of taking out a zero-interest loan when you could pay off your remodel in full include:

- The opportunity to put that cash in a high-interest savings account or investment portfolio in order to grow your money while you pay off your remodel in installments

- The opportunity to build a better credit score by paying off a loan on time and without penalties

- More wiggle room to cover emergency costs if they arise

How Can I Improve My Credit Score Before a Remodel?

What if you are struggling to get approved for bathroom remodel financing, or you want to qualify for a better loan? If your credit score is in the poor range (as opposed to fair or better), it may be worthwhile to try to improve your credit score before you start your remodel. Here are a few ways to do so.

Investigate Your Credit Report

When was the last time you actually looked at your credit report? There are free services like Experian that allow you to check your credit without penalty. Not only does this allow you to see where you stand with financial institutions and possible areas of improvement, but it also enables you to catch any fraudulent activity that is dragging down your credit score.

Improve Your Debt-to-Income Ratio

Have you been neglecting any outstanding loans or credit card bills? The best way to start improving your credit is to pay down your existing debt. This may require tight budgeting in the coming months, but it’s worth it to improve your debt-to-income ratio.

Schedule Your Payments

Maybe the issue hasn’t been that you don’t have the money to make payments toward existing debt. Instead, you’ve just been forgetful about due dates. Wherever possible, schedule monthly payments towards things like loans or credit cards. That way, you won’t be penalized for late payments.

Be Mindful of New Credit Inquiries

Hard credit checks (aka hard inquiries) happen any time you open a new line of credit, whether that’s a new credit card or a new home improvement loan. Hard credit checks can bring down your credit score for about six to twelve months. If you’re trying to improve your credit score quickly, try to avoid hard credit checks for the next six months.

Use Credit Strategically

If relying too much on credit brings down your credit score, shouldn’t it be beneficial to keep those credit cards tucked away? Believe it or not, your credit score can suffer if you have very little credit history to pull from. If you don’t have existing debt but you need to improve your credit score, start putting strategic purchases on your credit card and paying off your credit card bill on time.

Is Now the Right Time for a Bathroom Remodel?

A bathroom remodel is in your future, whether you’re ready to sign a contract today or six months from now. With this guide, you can start building the credit score you need to secure the financing that works best for your family.

At ZINTEX Remodeling Group, we strive to help homeowners secure a financing plan that makes bathroom remodeling accessible. To learn more, take a look at our guide to bathroom remodel financing.

.png?width=1280&height=720&name=Red%20And%20Black%20Modern%20Tips%20%26%20Trick%20YouTube%20Thumbnail%20(8).png)

{kind=link}